Business owner to business owner: If you’ve built your electrical, plumbing, HVAC, or other business from the ground up, handled difficult customers, and managed cash flow through tough times, you probably think you can handle whatever comes next, right?

It’s easy to feel like the earth-shattering things won’t happen to you…until they do.

Like it did for David, an electrical contractor who spent 15 years building his business to $2.8 million in revenue. When he suffered a heart attack on a job site at 52 years old, everything he'd built was suddenly at risk.

Your Business Is Your Greatest Asset — And Your Greatest Risk

David's story illustrates a critical reality: for most business owners, 70-80% of their net worth is tied up in their company. Your business is your livelihood as much as it's your retirement plan, your family's security, and your legacy. But this concentration of wealth creates enormous vulnerability.

How to Safeguard Your Most Valuable Asset

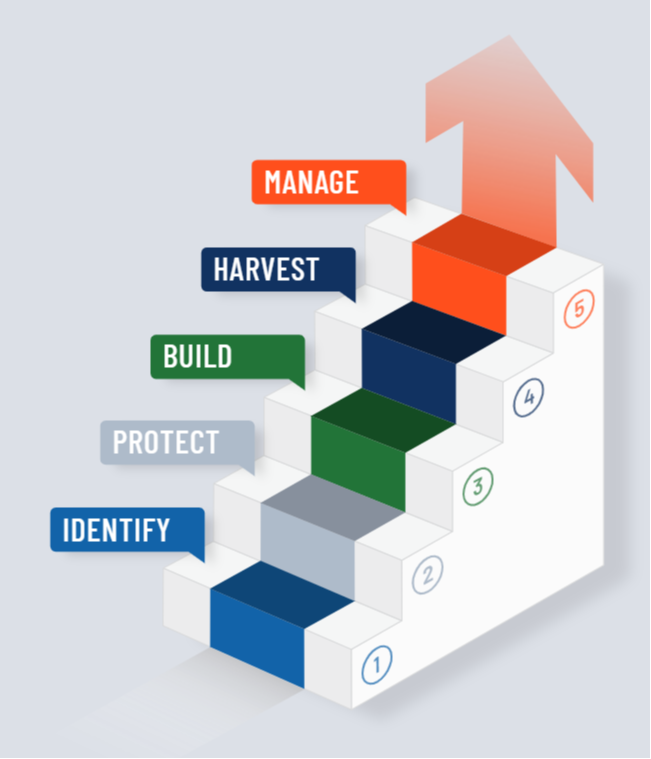

I’ve spent decades helping business owners build and protect wealth —all with the help of the Five Stages of Value Maturity framework:

These five stages create a roadmap for systematically building and harvesting the value in your business.

Stage 1 is about identifying your business value and wealth gaps. Today, I’m going to talk about stage 2: Protect. Because knowing what your business is worth means nothing if it can disappear overnight.

The 5 D's That Threaten Your Business

Every business owner should know the following five catastrophic factors that can destroy value almost instantly. They’re known as the "5 D's":

1. Death

What happens when you die unexpectedly? Your family faces an impossible choice: drain personal resources to keep the business alive or sell quickly at whatever price they can get. Without proper planning, your profitable business becomes worthless to the people you're trying to protect, and your legacy can suffer greatly.

2. Disability

This one hits trade businesses particularly hard. Your body is how you built this business. But what happens when you can't work for six months? David found out the hard way when his heart attack left him unable to run jobs or manage his 12 employees.

3. Divorce

I’m grateful to be happily married — for more reasons than one! A messy divorce can force you to sell your business to divide assets or saddle your company with debt to buy out your spouse interests. I've watched profitable trades businesses collapse when divorce proceedings exposed them to claims from non-involved spouses.

4. Distress

Market downturns happen. Major customers leave. Supply chain issues emerge. When financial pressure hits, do you have reserves to weather the storm, or will you be forced to liquidate equipment and lay off trained employees?

5. Disagreement

Maybe you have a partner. Maybe key employees know where all the customers are. What happens when relationships go bad? Without clear agreements and documented processes, personal conflicts can easily become business disasters.

How Exposed Are You to Risk?

David's heart attack exposed the protection gaps that plague most trade business owners. Like many successful contractors, he thought basic life insurance and workers' compensation meant he was covered. The reality revealed something different:

- No disability insurance covering his $140,000 salary and distributions

- Business overhead expenses that would drain cash reserves in 6 weeks

- Client relationships that existed only in his head

- No buy-sell agreement with his 25% partner

- Systems and processes known only to him

Sound familiar? Many trade business owners I meet have similar gaps.

How to Create a Foundation of Protection

Here's how to build real protection for your business to help prepare you for common risks and anything else life throws your way:

Insurance Coverage

Disability Insurance: Consider both personal income replacement and business expense coverage. When you can't work, your mortgage payment doesn't stop, and neither do your business loan payments, key employee salaries, or equipment leases.

Key Person Life Insurance: Protects your business if you die and funds buy-sell agreements if you have partners.

Liability Coverage: Your industry has specific risks. Make sure your coverage matches your actual exposure, including umbrella policies to protect personal assets.

Business Continuity Planning

Document Your Systems: Write down how your business runs. Client contact procedures, project management workflows, vendor relationships. If something happened to you tomorrow, could someone else run your business using written instructions?

Cross-Train Employees: Stop being the only person who knows critical information. Train others to handle key accounts, manage projects, and maintain customer relationships.

Build Company Relationships: Your biggest customers should know other people in your organization, not just you. This protects against client loss if something happens to you.

Financial Reserves: Maintain cash to cover at least three months of expenses without new revenue so you have options should problems arise.

Legal Structures

Buy-Sell Agreements: If you have partners, define exactly what happens when someone leaves, becomes disabled, or dies. Include how you'll value the business and fund the buyout.

Employment Contracts: Key employees should have agreements that protect your investment in them and prevent them from taking customers if they leave.

Asset Protection: Structure your business to shield personal wealth from business liabilities.

Don't Wait Until It's Too Late

Every month you delay implementing proper protection, you're exposed to unnecessary risk. Your health can change. Market conditions can shift. Business relationships can sour. But you can control your protection strategy right now, while you have leverage and options.

Ready to Protect Your Business and Create Value?

At Harford Financial Group, we help you implement protection strategies that do more than prevent disasters — they create business value. Buyers pay premiums for businesses with proper systems and reduced risk. When you follow the complete Five Stages framework, protection becomes the foundation for building and harvesting maximum value.

Ready to assess your protection gaps? Schedule a consultation to evaluate your current coverage and design a comprehensive protection strategy that lets you pursue growth with confidence.